Co-Lending: Can We Fix the Friction?

- Fastest growing loan categories

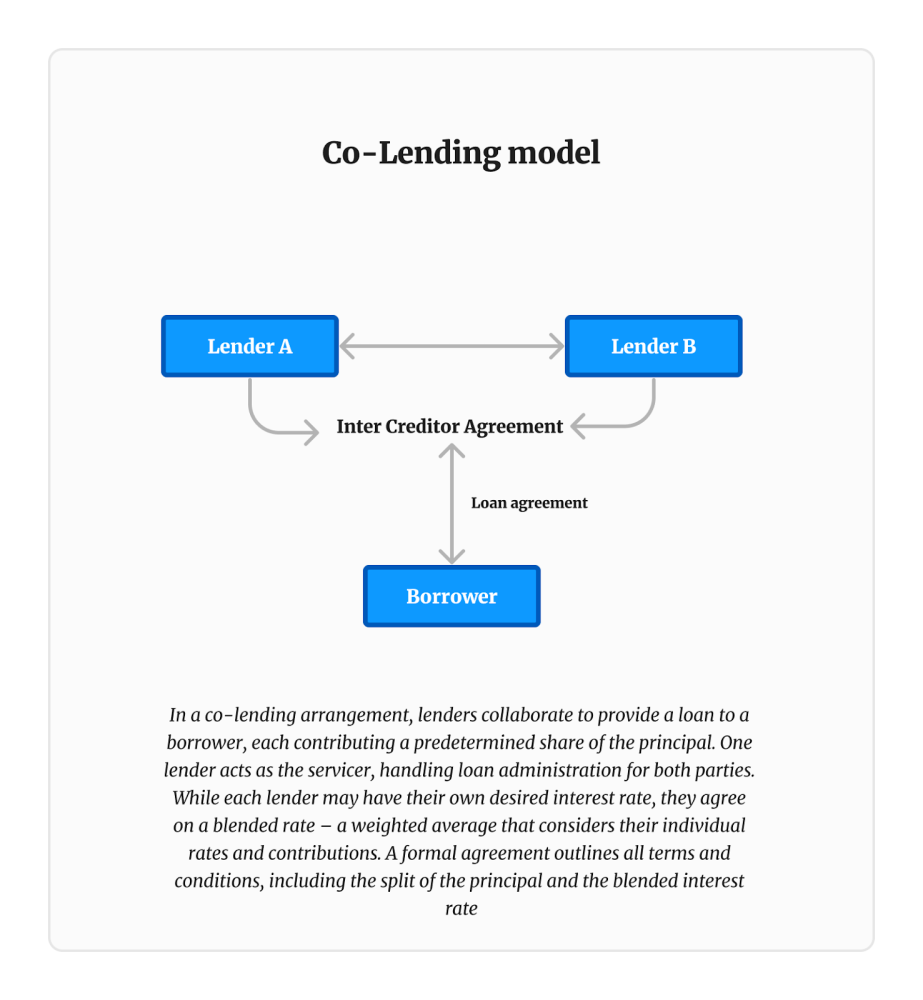

- Co-lending Model

- How it works?

- Bridging the Gaps

- What do you think?

One of India's fastest-growing loan categories right now is relatively unique to this market - Co-lending. Last week rating agency CRISIL flagged that Co-Lending has witnessed a phenomenal rise and is set to be a USD 12 Billion Loan book by this June.

What is behind this growth? India’s co-lending history might give you some context…

Co-lending in India is fascinating. It emerged around 2014, a decade after the country's financial sector underwent significant liberalization. This period saw a surge in capital market activity, but credit flow to crucial sectors like agriculture and small businesses remained sluggish. This was partly due to a long-standing Priority Sector Lending (PSL) regulation. Here's the thing about PSL: it mandates banks to allocate a portion of their loans to these very sectors, which are considered essential for the economy's development but often deemed riskier by banks. Meeting these PSL targets proved inconsistent for banks.

Enter Non-Banking Financial Companies (NBFCs). These nimble players, often with deep regional roots and expertise in specific borrower segments, were well-positioned to serve the underserved. However, their ability to expand was limited by access to affordable capital. This is where co-lending emerged as a win-win solution. Banks could leverage NBFCs' reach and expertise to fulfil their PSL obligations, while NBFCs gained access to cheaper funds from banks to fuel their growth.

The story doesn't end there. The rise of fintech companies (mostly digital lending focused) soon after, further amplified the co-lending opportunity. Fintechs brought automation, data analytics, and a digital-first approach to the table, streamlining loan processes and making credit assessment more efficient. This three-way collaboration – banks, NBFCs, and fintechs – became the recipe for co-lending's success in India.

Essentially, co-lending enhances financial stability by enabling risk sharing between two institutions and (often) subjecting borrowers to dual scrutiny and integrating stringent compliance and risk management practices.

The mandatory risk-sharing, means both parties retain stakes in the loans (usually the bank funds 80% and the NBFC funds the other 20%), aligning assets and liabilities to avoid management pitfalls

While the co-lending model is unique to India, it varies in its implementation globally. Take The "Fannie Mae's Small Loan Program" in the US - it involves a partnership between Fannie Mae and local lenders to offer financing for smaller multifamily properties. This co-lending arrangement leverages government backing and local market insights, enabling loans that might be considered too risky or small for individual lenders to manage alone.

In the European Union, the European Investment Bank (EIB) collaborates with local banks in several countries to fund projects that align with EU goals, including innovation, environmental sustainability, and infrastructure improvements. The EIB contributes to these loans on favourable terms, thereby reducing the financial risk and burden for local banks.

The core principles of this collaborative lending model are the same across the globe - collaboration between different financial entities consistently aims to enhance economic opportunities and financial inclusivity.

And it works..

Take NBFC X for instance (one of the largest Non-Bank Financial Companies in India). By strategically partnering with digital platforms, fintechs, and banks, NBFC X was able to streamline loan origination, particularly for personal and business loans. This not only helped them expand their customer base but also achieve higher returns on equity compared to traditional lending models.

Despite incurring operating costs, this model yields a higher RoE compared to traditional lending approaches due to reduced credit costs and capital requirements.